Flow-through Trends Investors Must Know with Canada’s Largest ExploreCo Funder Lisa Davis

The Canadian Flow-Through Share tax regime was established in the 1970s to promote exploration investment in Canada. Resource issuers can “flow through” the tax deductions and credits associated with the issuers’ exploration activities to the first subscribers of these common shares. In 2007, PearTree developed the highly successful Flow-Through Share Donation Platform (FTSDP), resulting in increased philanthropy and expanded value access for global investors.

Flow-Through Shares allow donors to purchase shares of Canadian resource companies and donate them to charity, reducing their taxable income, supporting non-profits, and accelerating the development of resource projects in Canada.

Learn MorePearTree’s Flow-Through Donation Financing is uniquely consistent with CRA and Revenu Quebec’s advance tax rulings and Technical Interpretations.

Learn More

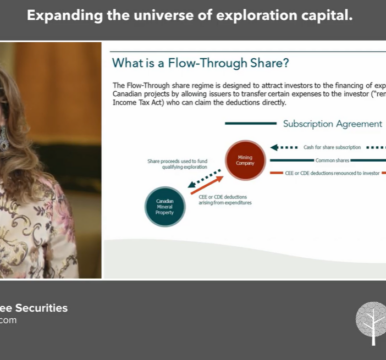

FLOW-THROUGH SHARES EXPLAINED

Source: PDAC – for more detailed analysis Visit the PDAC website

Want to learn more about how flow-through shares work and how they can benefit you? Contact us at info@peartreecanada.com for more information.

PearTree accelerates significant gifts for charitable organizations via our Flow-Through Share Donation Platform (FTSDP).

Because PearTree’s philanthropic business activity is assisting charities and donors, we help donors achieve a lower after-tax donation cost, leading to more transformational gifts for your charity. We help donors give more for less.

For more information on how PearTree supports charities through our Flow-Through Share Donation Platform, contact info@peartreecanada.com.

PearTree significantly reduces the after-tax cost of giving via our Flow-Through Share Donation Platform (FTSDP), so you can increase or accelerate your philanthropy.

Donors can expect the average after-tax cost of their charitable giving to be less than 10% in most Canadian provinces.

To learn how PearTree can help you amplify your giving and reduce your after-tax cost of donation, contact us at info@peartreecanada.com.

PearTree delivers an array of measurable value to resource issuers, such as:

Reach out to info@peartreecanada.com for more information.

Each donation transaction is tailored to donors in specific provinces. PearTree closes approximately 60 financings annually funding about $ 500 million in flow-through share financings sourced for donation purposes. However, financings are dependent upon the public markets and factors including commodity prices which are volatile. As such, we recommend that our clients inform us of their donation requirements as soon as possible and to participate as early in the year as possible. Q1 is the busiest time for financings.

To discuss your donation goals, contact us at info@peartreecanada.com.

Canadian tax authorities are fully onside with this structure. In over 15 years and over 500 financings and in thousands of client tax returns there has never been a single instance where the CRA or a provincial tax authority has questioned or challenged the appropriateness of this arrangement. Early on PearTree obtained Advance Income Tax Rulings from the CRA and Revenu Quebec in which the authorities confirmed the tax consequences.

There is also no equity price risk because the shares are sold on closing. If the sale is not consummated the transaction is cancelled and subscription funds returned to the subscriber. That said we have never had a situation where a financing has not closed due to the liquidity provider not performing. There is a tax risk albeit limited. For tax purposes a flow-through share behaves like a limited partnership unit in that the resource issuer must spend the funds for specific purposes as set out in the tax legislation, the biggest single cost being drilling core samples. If the funds are not properly spent the CRA may reassess the donor subscriber.

In 500 financings we have had 6-7 instances where there is a dispute with the CRA but in every case the PearTree donor subscribers were made whole under the indemnity provisions imbedded in every transaction.

If you’d like to better understand the process and safeguards for donors, our team can help. Reach out at info@peartreecanada.com.

The charity provides a Fair Market Value receipt for the share equal to the cash received on closing. There is no valuation risk and the charity will not accept the gift of shares unless the shares are sold on closing. As a result, both the donor and the charity know with certainty that the pledged gift amount will be received by the charity.

For additional details on how PearTree minimizes risk for charities, please contact info@peartreecanada.com.

Alternative Minimum Tax (AMT) is a feature of the Income Tax Act designed to ensure that all taxpayers remit a minimum amount of tax relative to income in any one year, even though you may have participated in tax incentive transactions such as Flow Through Share subscriptions which would otherwise reduce your taxable income to nil. AMT is a timing issue and the Flow Through expenses reflected in our analyses can be carried forward indefinitely against all future income sources including deemed dispositions on death. Note: AMT is not applicable in the terminal year. Donation receipts can be carried forward for five years. Donors should consult their tax advisor about AMT.

For additional information about how income levels and AMT considerations may impact participation, contact info@peartreecanada.com.

There is no risk to the Canadian resource issuer. The issuer is simply issuing flow-through shares for subscription by our donor clients.

To learn more about how PearTree supports Canadian resource issuers with flow-through share financings, contact us at info@peartreecanada.com.

Interested parties should contact a PearTree representative for more information or email us at info@peartreecanada.com.